Listen to the latest episode of Ghost Wrap here, brought to you by Mazars:

Bell Equipment: let’s talk about cash, baby (JSE: BEL)

Specifically, where did it go?

The Bell Equipment share price has had quite a year, posting a year-to-date increase of 23.7% according to Google Finance. The share price has shot straight up this month, which leaves it vulnerable to a correction and consolidation.

After the release of trading statements caused all the buzz, the release of detailed results didn’t add to the party. In face, the share price was slightly down on the day.

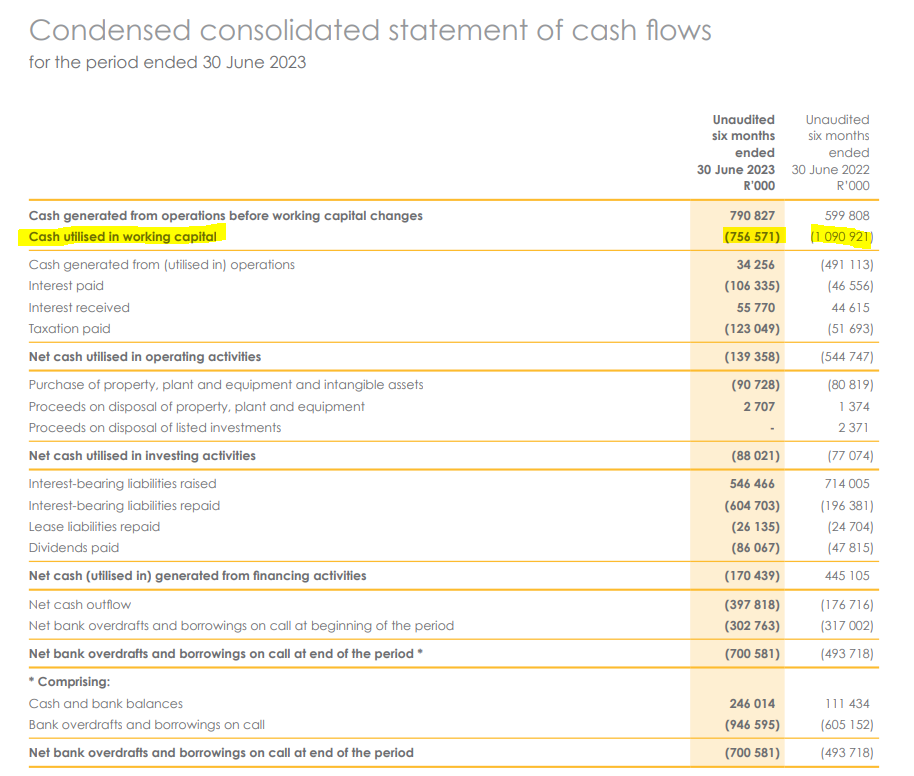

The metrics certainly look good, with revenue for the six months to June up by 42% and HEPS jumping 63%. Cash is important too, with that metric telling a very different story.

Despite profit from operating activities of R535.9 million, the cash outflow for the period was nearly R398 million. Last year, profit was R308 million and the cash outflow was R177 million, so this mismatch isn’t anything new.

The culprit is right at the top of the cash flow statement, with almost all the cash generated in this period being sucked into working capital. At least it’s better than last year:

The inventory balance has jumped from R4.75 billion to R5.88 billion. This is based on a planned increase in production volumes and shipping delays from South Africa. If you exclude inventory, Bell’s balance sheet isn’t exactly cash flush. It’s not in bad shape, but investors will keep a close eye on working capital.

There is no interim dividend once again, which makes sense in the context of the balance sheet.

City Lodge occupancies are ahead of 2019 levels (JSE: CLH)

But room rates haven’t recovered yet, so pricing power remains a concern

Group occupancy at City Lodge is up by a whopping 18 percentage points year-on-year, coming in at 56% for the year ended June 2023 vs. 38% in the prior year. Importantly, this is now slightly ahead of 55% in the FY19 result before the pandemic slaughtered the industry.

Although average room rates are up 12% vs. last year, they remain below pre-Covid levels. Pricing power to fill the hotels is in doubt here. What isn’t in doubt is the success of the food and beverage strategy, now contributing a significant 17% of total revenue (up from 15% last year). With load shedding as an ongoing reality for all of us, giving people a place to work and eat really isn’t a bad approach in this market, even if they don’t stay the night. The gross profit margin on food and beverages improved from 55% to 58% year-on-year.

As great as that is, it will be important to the investment case that room rates make a full recovery as well. The inflationary pressures in the cost base are substantial, with property costs up by 19%. The fixed cost base isn’t static.

Still, EBITDAR (the “R” isn’t a typo – this is industry standard in hospitality) increased by 83% and EBITDAR margin increased from 27.5% to 32.4%.

Thanks to a vastly improved balance sheet, a dividend of 8 cents per share has been declared. This is despite a significant capital investment programme in the new financial year with a clear focus on renewable energy solutions. They even need to put in place water solutions at some of the facilities, as supply can be erratic.

The good news for the new financial year is that occupancy has run at over 60% since the end of the financial year. The warm weather has only just begun, so hopefully a strong few months are ahead.

The share price hasn’t moved much based on these earnings. I think the market is keeping an eye on return on assets and the pricing power concerns I’ve highlighted.

Metrofile is swimming upstream (JSE: MFL)

If you love picking up coins in front of a steamroller, this one is for you

Metrofile isn’t exactly the most exciting company around. Image processing and document storage isn’t high on the list of “things I want to do when I grow up” for most people. The latest numbers won’t do anything to change that.

Excluding the acquisition of IronTree Internet Services, revenue has increased by 13%. Including that acquisition, revenue is up by 16%. That sounds pretty good, but wait until the bottom of the income statement. Before we move away from revenue, it’s important to note that gross box volumes intake was 6% and destructions and withdrawals were 9%, so closing box volumes fell by 3%.

Operating profit only increased by 6%, with margin mix as a concern because image processing is lower margin than other sources of revenue. There are obviously also inflationary pressures on costs. The company has invested in its go-to-market sales team, so more money is being put behind marketing to try and turn the tide on the drop in volumes.

Net debt increased by 11% and net finance costs were 18% higher because of the increase in prevailing interest rates. This is why HEPS could only limp 5% higher. The dividend for the year of 18 cents was consistent with the prior year, so the payout ratio dipped.

On a share price of R3, that’s a dividend yield of 6%. This means that the market is expecting the company to deliver meaningful growth in HEPS. Although this period wasn’t exactly a thrill ride, the company has highlighted important contracts in South Africa and the UAE that have been won.

The share price performance over 5 years is slightly in the red, so investors have had to be content with dividends over that period. The share price is down 14% this year.

Sun International confirms that we are still jolling (JSE: SUI)

South Africans know where the party is

Even load shedding couldn’t stop the Sun International party in the six months to June 2023, with income up 11.7% and adjusted EBITDA up by 5.6% thanks to diesel costs and a stronger contribution from resorts and hotels, which is a lower margin business (22% in this period) than gaming. Although margins are under pressure, this is a positive change in profits and that’s good going in this environment. Group adjusted EBITDA margin fell from 28.7% to 27.2%. Without load shedding, it would’ve fallen to 28.2% instead.

Adjusted headline earnings per share tells a better story, up 10.1%. When you consider the backdrop against which this result has been achieved, it looks pretty decent. The market certainly thought so, with the share price trading around 6% higher by lunchtime.

The major driver wasn’t gaming revenue, which contributes 78% of group income. It grew 6.6%, with casino income up 3.2% and Sun Slots slightly down year-on-year because of load shedding. SunBet generated record income, up 138.4% year-on-year. If you are willing to place much reliance on management’s calculation of adjusted EBITDA, then SunBet is up from R14 million to R90 million as income has moved significantly above break-even level. The company recognises that SunBet operates in a highly competitive industry and the hope is to differentiate through SunBet being part of the wider Sun International offering. They are aiming for 10% market share in online betting by 2026.

The real winner was resorts and hotels, up 26.9%. People are clearly hungry for experiences in a post-pandemic world and the weak rand really helps. Not only does it make us more appealing as a global destination, but it also means that locals who used to be able to afford an overseas holiday can now only afford to take a Sho’t Left. Average occupancy increased from 57% to 66.8%.

South African debt sits at R5.9 billion which is in line with December 2022 levels. Debt to adjusted EBITDA is at 1.8 times. Net interest jumped by 40.3% as the prevailing interest rates have increased substantially. With debt to adjusted EBITDA below the target of 2.0 times, a dividend based on 75% of adjusted HEPS has been declared. This is an interim dividend of 148 cents.

The outlook for the remainder of this year is bullish, which would also have been a contributor to the positive share price response.

Hurwitz didn’t survive the Transaction Capital mess (JSE: TCP)

Jonathan Jawno is back in the hot seat to try and fix this nightmare

I must say, I was skeptical about David Hurwitz managing to survive the SA Taxi debacle with his group CEO role still intact. We now have the answer, as he will step down effectively from 31 December 2023 and will remain available in 2024 to ensure a smooth handover. It sounds like 2024 will be gardening leave for him, so life could be worse.

The Transaction Capital garden isn’t looking so good and the share price performance on Tuesday morning is likely to be ugly. Aside from the catastrophe at SA Taxi, WeBuyCars expects earnings to be approximately 20% lower year-on-year, with a notable decision not to open any new branches in the second half of the 2023 financial year. Nutun’s earnings are growing more slowly than previously communicated. At a time when the group desperately needed the other divisions to do well or even outperform, it just hasn’t played out that way.

This brings us neatly to SA Taxi, with that segment renamed Mobalyz in an effort to get us to forget about how bad things are. There have been significant restructuring activities, moving towards a more variable cost model to help the group weather the storm. This results in savings of R500 million per year. Credit is being tightened and operations are being simplified, with the auto refurbishment and repair facilities potentially being sold. The business really has fallen apart, with short-term tactics to improve cash flow that definitely reduce the strategic moat over the long-term.

Aside from Jonathan Jawno who is spearheading the SA Taxi restructure, Chris Seabrooke is now chairing a Mobalyz Debt Sustainability Committee as Sabvest has a significant stake in Transaction Capital. It really is a case of all hands on deck.

Get ready for the share price to Mobalyz itself, firmly in the wrong direction again.

Transpaco agrees to a big repurchase at a discount (JSE: TPC)

This actually shows you how hard it is to sell a large stake in a local small- or mid-cap

Manufacturers Investment Company (Pty) Ltd is a private company that holds a meaningful stake in Transpaco. As liquidity in this stock is low, it’s just about impossible to sell a stake this size without bombing the share price of the company is the process. Welcome to life in local small- and mid-cap companies.

Transpaco is wise to the opportunity to provide exit liquidity to this shareholder in a form of a specific repurchase. Of course, this is at a discount to the current share price, so it’s a win for the remaining shareholders.

The stake represents 3.67% of shares outstanding and the cash consideration for the repurchase is R30.6 million. The price is R27.83, which is a 10.10% discount to the 30-day VWAP calculated based on Friday 1 September. The current share price is R33.76 but this is where a VWAP is so important, as illiquid stocks can move by large percentages on thin volumes. A VWAP takes that into account (as this is a volume-weighted calculation).

A circular will be sent to Transpaco shareholders to approve the proposed buyback.

Little Bites:

- Director dealings:

- Des de Beer has bought another R17 million worth of shares in Lighthouse Properties (JSE: LTE).

- A director of AngloGold Ashanti (JSE: ANG) purchased American Depository Receipts worth $33k.

- The Blue Label Telecoms (JSE: BLU) story continues to divide the market. A director of a subsidiary selling shares worth R97k doesn’t do any favours for sentiment.

- We don’t know what transaction Clientele Limited (JSE: CLI) is contemplating, but we know that negotiations are still alive and well because a further cautionary announcement has been issued.

- There’s still no sign of financials at Salungano (JSE: SLG), as the audit process cannot be completed until the refinancing process has been concluded. One of the conditions of the refinancing process is the appointment of a Chief Restructuring Officer, which tells you how things are going. No timing has been given in the announcement for the release of financial results. The shares remain suspended from trading.

- Imtiaz Patel is stepping down from the board of MultiChoice (JSE: MCG), where he currently serves as Chair. Elias Masilela will take on that role, having already been on the board as an independent director for a while. Importantly, Patel will continue consulting to the group until 2028, with specific involvement in ShowMax and SuperSport. Although institutional knowledge is important in any organisation and Patel has plenty of that, this does also raise some questions around succession planning and the depth of talent in the group.

- Advanced Health (JSE: AVL) announced that all conditions for the clean-out dividend of 20 cents per share and scheme of arrangement at 80 cents per share have been met.

- Tsogo Sun (JSE: TSG) repurchased shares to the value of nearly R1.8 million in the odd-lot offer.

Can we please get a comment on Altron

Hi Farouk. I comment on the news that comes out each day. No release on SENS by Altron = no comment unfortunately.